Key Takeaways

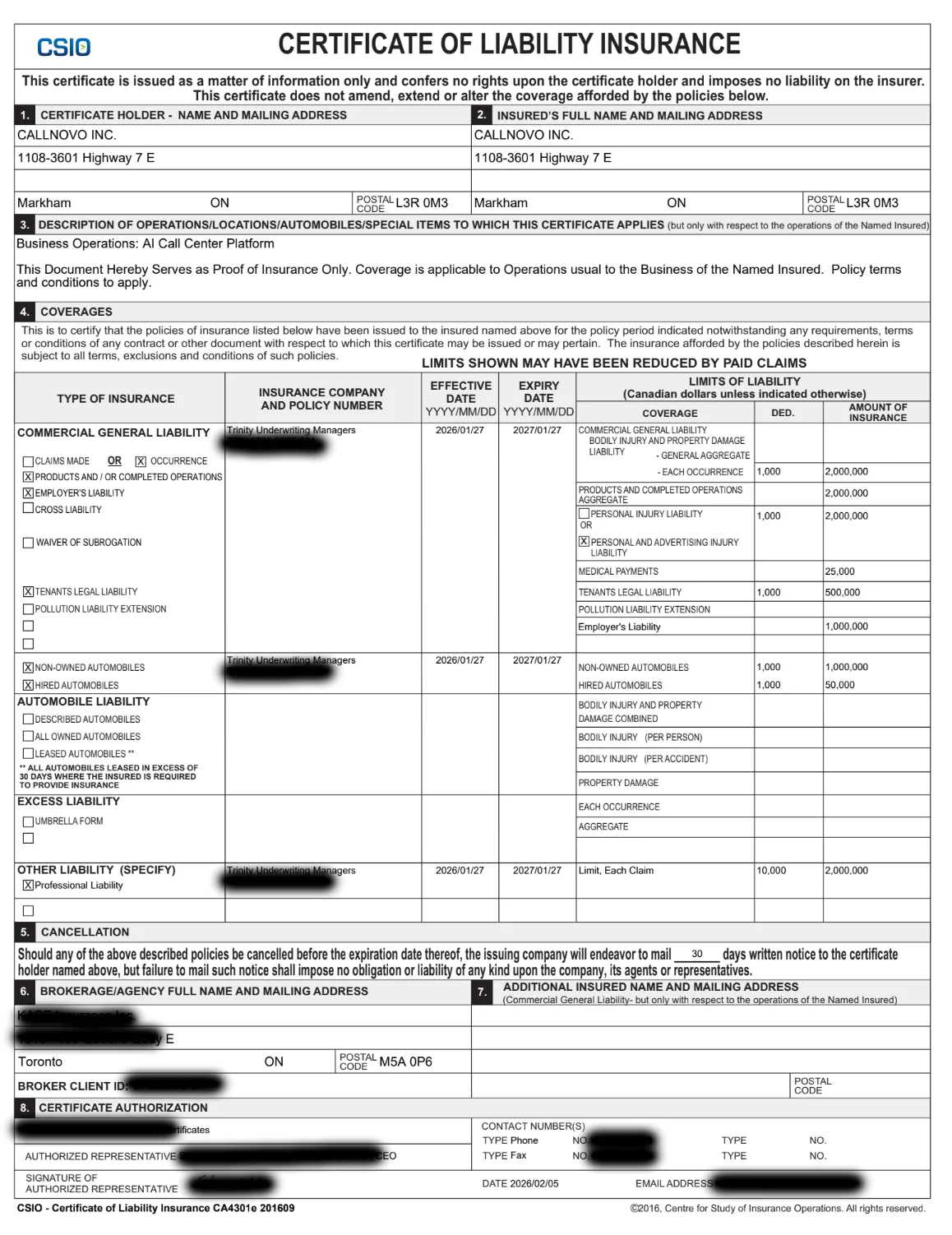

- Callnovo carries multi-million dollar Professional Liability (E&O) and Commercial General Liability coverage — Underwritten and active, covering our operations including general liability and cyber risk. Not a generic policy. Not a checkbox.

- Most BPO companies don’t carry Professional Liability insurance at all — E&O coverage for customer service outsourcing is still uncommon in the industry. If your provider can’t show you a certificate, ask why.

- Insurance isn’t just about covering mistakes — it’s a signal of how a company operates — Companies that invest in proper coverage tend to also invest in proper security, proper training, and proper processes. The insurance is the visible part of a deeper commitment.

- You should be asking every outsourcing vendor for proof of insurance — It’s one of the fastest ways to separate serious operators from companies running on hope.

The Question Nobody Asks During Vendor Selection

When companies evaluate BPO partners, the checklist is predictable. Pricing. Languages. Time zones. Technology stack. Maybe a reference call or two.

Almost nobody asks: “Can I see your certificate of insurance?”

We know, because we’ve been on hundreds of those calls. Clients ask about our agent training programs, our QA processes, our AI capabilities — all reasonable questions. But the question that would tell them more about our operational maturity than anything else rarely comes up.

So we decided to talk about it ourselves.

What We Carry and Why

Callnovo carries comprehensive liability coverage designed for our operations, covering general liability and cyber risk. Here’s what it includes:

Professional Liability (Errors & Omissions) covers claims arising from professional services — if a process error causes a client financial loss, or if a service failure leads to damages. This is the coverage that matters most in our industry, and it’s the one most BPO companies don’t carry.

Commercial General Liability covers bodily injury, property damage, and personal/advertising injury. It’s standard for any serious business, but “standard” doesn’t mean universal in the BPO world — especially among offshore-only operators.

Employer’s Liability covers claims from our own workforce. With 2,500+ agents across multiple countries, this isn’t optional — it’s essential.

Our policy is occurrence-based, not claims-made. That distinction matters: occurrence-based policies cover incidents that happen during the policy period regardless of when the claim is filed. It’s broader protection, and it costs more. We chose it deliberately.

Why Most BPOs Don’t Have This

Let’s be honest about the industry. The majority of BPO companies — particularly small to mid-sized offshore operators — don’t carry professional liability insurance. There are a few reasons:

Cost. Comprehensive E&O and cyber coverage for a customer service operation isn’t cheap. The premiums reflect the risk profile of handling customer data and operating across multiple jurisdictions. Many BPOs operate on thin margins and view insurance as an expense they can avoid.

Availability. Underwriters are still catching up to outsourced customer service as a risk category. Finding a carrier willing to write a policy that explicitly covers BPO operations — not just generic “consulting services” — requires specialized brokers and specialized markets.

The “it won’t happen to us” problem. Small BPOs tend to assume that if something goes wrong, they’ll work it out with the client. That works until it doesn’t. One significant data handling error, one cyber incident, one process failure that costs a client a major account — and suddenly the conversation shifts from customer service to lawyers.

We don’t operate on hope. We operate on coverage.

What This Means for Our Clients

When you work with Callnovo, our insurance coverage means three practical things:

1. Risk transfer. If our service causes your business a covered loss, there’s a professional liability policy backing the resolution — not just a promise. You’re not depending solely on our balance sheet or goodwill.

2. Contractual compliance. Many enterprise procurement teams require vendors to carry minimum insurance thresholds. Our $2M coverage meets or exceeds the insurance requirements in most enterprise vendor agreements. If your legal team requires a certificate of insurance, we can provide one within 24 hours.

3. Operational signal. Companies that invest in proper insurance tend to invest in proper everything else. Our coverage sits alongside our Bitdefender endpoint security across 2,500+ devices, our fraud prevention protocols, and our internal compliance processes. Insurance isn’t a standalone decision — it’s part of how we run the business.

The Uncomfortable Truth About Outsourcing Risk

Here’s what nobody in the BPO industry wants to say out loud: when you outsource customer service, you’re handing a third party the power to damage your brand, lose your customers, and mishandle sensitive data. You’re transferring the work, but unless your vendor is properly insured, you’re keeping all of the risk.

That asymmetry is the real problem. Most outsourcing contracts include indemnification clauses, but indemnification is only as strong as the company behind it. A 50-person offshore BPO can promise to indemnify you for $5 million in damages, but if they don’t have the assets or insurance to back it up, that clause is a piece of paper.

Insurance changes that equation. It means there’s a third party — the underwriter — standing behind the promise. It means claims get paid even if the vendor has a bad quarter. It means the coverage was evaluated, priced, and approved by professionals whose entire job is assessing risk.

We carry insurance not because we expect things to go wrong. We carry it because we take seriously the trust our clients place in us, and we believe that trust should be backed by more than words.

Ask Your BPO Provider These Three Questions

If you’re currently working with an outsourcing partner — or evaluating one — here are three questions worth asking:

-

“Do you carry Professional Liability (E&O) insurance?” — If the answer is no, or vague, that tells you something important. If the answer is yes, ask for the certificate.

-

“Does your policy specifically cover your AI/automation operations?” — Generic policies may exclude AI-driven services. Make sure the coverage matches what they actually do.

-

“Is your policy occurrence-based or claims-made?” — Occurrence-based provides broader protection. Claims-made is more common (and cheaper) but leaves gaps if the policy lapses.

You wouldn’t hire a contractor to renovate your office without verifying their insurance. The same standard should apply to the company handling your customers.

About Callnovo

Callnovo is a global multilingual BPO with 2,500+ agents, 65+ language capabilities, and delivery centers across Asia and Latin America. Our operations are backed by comprehensive Commercial General Liability and Professional Liability insurance, Bitdefender enterprise endpoint protection, and internal security protocols designed for enterprise-grade client requirements. Learn more at callnovo.ai.